As Greek

Prime Minister Alexis Tsipras braces for another round of tough negotiations

with creditors, savers are still reluctant to bet their money that this year’s

talks will be less perilous for their country’s place in the euro area than

2015.

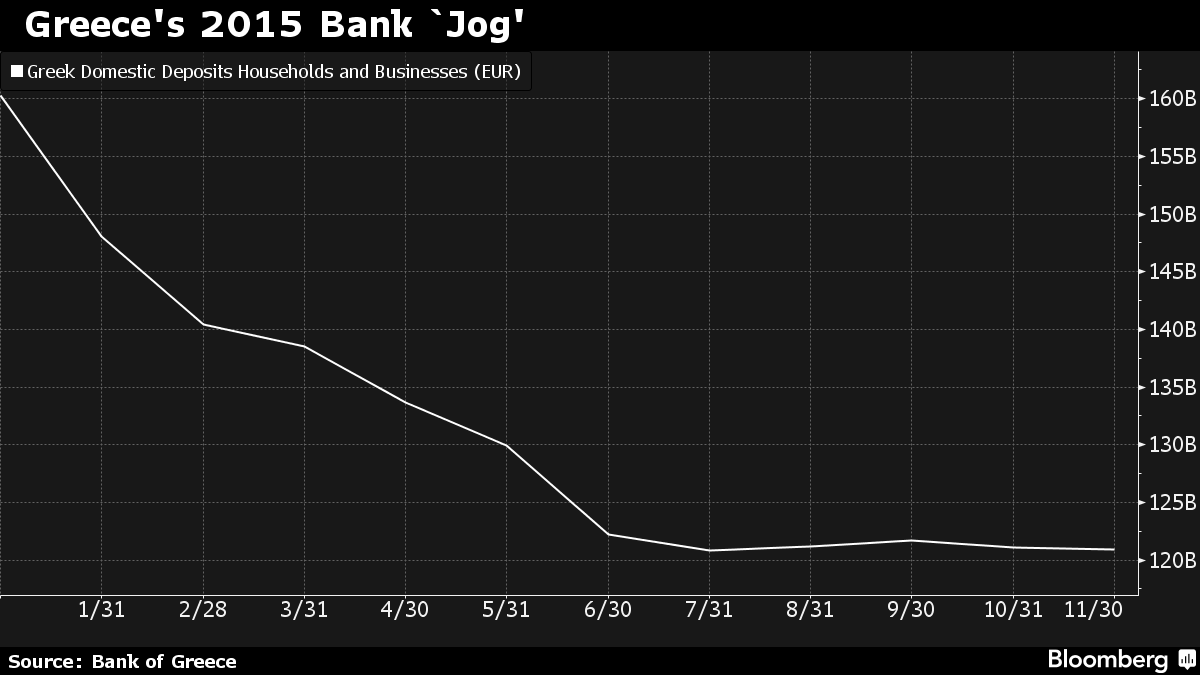

Deposits held by households and businesses

in Greek banks fell close to a 12-year-low of 120.9 billion euros ($131.3

billion) in November, bringing total losses to a record of more than 43 billion

euros, or 26.4 percent of total savings, in the last 12 months.

Savers’ distrust may derail the government’s

goal of lifting capital controls by the end of June. Reluctance to return

deposits held abroad or under mattresses back to banks hinders the ability of

lenders to provide credit to the economy, as the government struggles to lead

Greece out of recession in 2016 after a turbulent year which pushed the country

to the verge of leaving the euro area.

Separate data also released by the Bank of

Greece this week showed that private sector deleveraging picked up pace in

November, with outstanding loan balances dropping 2.2 percent from the previous

year. Credit contraction “returned with a vengeance in July, continued unabated

in August, slowed in September, yet picked-up speed again in October and

November,” Athens-based Pantelakis Securities’ analysts Paris Mantzavras and

George Grigoriou wrote in a note to clients on Thursday.

Greek lenders cleared the hurdle of a

pan-European review in 2014 thanks to capital increases of more than 8 billion

euros and restructuring plans approved by the European Commission, only to see

their solvency put to the test in 2015 when Tsipras’s government revolted

against the terms attached to the country’s bailout lifeline. A stress test by

the European Central Bank uncovered a 14.4 billion euro-hole in their books,

amid increases in bad loans, subdued economic activity, expensive emergency

funding requirements and strict limits on capital transfers.

Private investors plugged most of the shortfall,

as bank stocks lost more than 93 percent of their value in 2015. The government

covered the rest with more than 5 billion euros of emergency loans from the

euro area’s crisis fund, while the valuation of the state’s equity portfolio in

Greek lenders was practically wiped out in November.

Even as Tsipras assures savers that the

country’s banks are now among the most adequately capitalized in Europe and

there’s no risk of haircut or re-denomination for deposits, Greeks are still

unwilling to bring their savings back, as the government remains at loggerheads

with creditors over demands for additional pension cuts. Pension savings is

among the main conditions for unlocking Greece’s next aid tranche and for

debt-relief talks between the country and its euro-area creditors to begin.

“We consider the recent successful

completion of the recapitalization of the Greek core banks as an important step

towards the restoration of the impaired depositor confidence,” Athens-based

Euroxx Securities’ analysts Yiannis Sinapis and Vangelis Karanikas wrote in a

note to clients on Thursday, adding that the process will be slow, subject to

political stability and the smooth implementation of the bailout agreement by

the government.

Πηγή: bloomberg.com

Δεν υπάρχουν σχόλια:

Δημοσίευση σχολίου